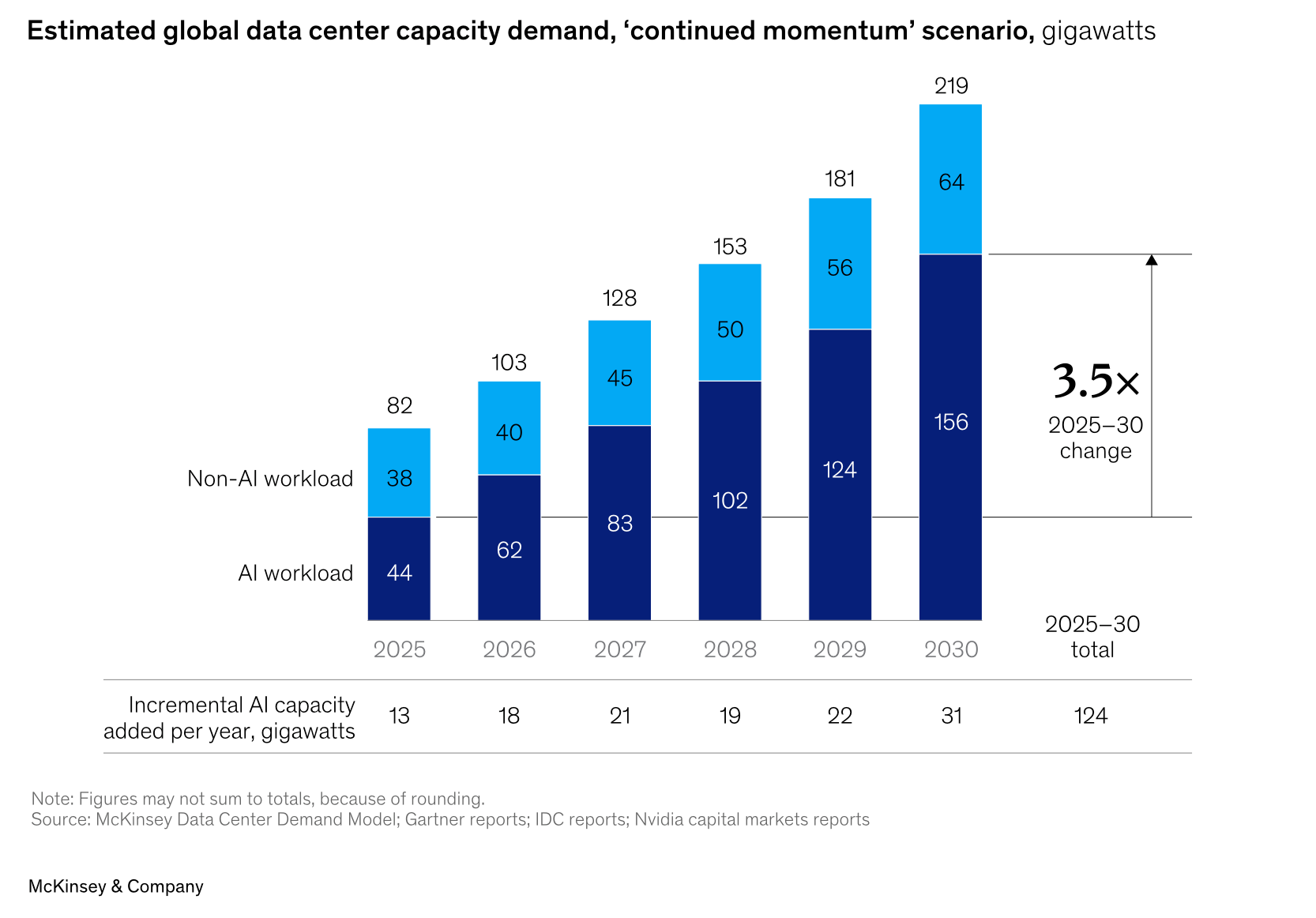

AI now dominates the conversation across technology, capital markets and government. It has been described as transformational, existential, inevitable and imminent, often all at once. Yet for all the noise, there remains significant uncertainty about where AI is truly heading, how quickly value will be realised, and what it genuinely demands from the infrastructure that underpins it.

That uncertainty extends to the United Kingdom’s role within it. The UK is unlikely, without major structural change, to compete as a global centre for large-scale AI training. Power costs alone make that improbable. But that does not preclude leadership. It simply defines where it must sit.

The UK possesses world-class research institutions, sophisticated financial markets, highly skilled technical talent and deep national data sets across healthcare, financial services, defence and public administration. With the right infrastructure and disciplined execution, those strengths can position the UK as a leader in applied AI, high-trust environments and inference-driven deployment. As AI use expands across enterprise and public services, inference infrastructure close to population centres will become increasingly critical. That is where the opportunity lies.

Clarity, however, has not yet matched ambition. AI leadership will not be delivered by announcement. It will be built through private-sector execution, focused capital allocation and infrastructure aligned to real use cases.

In 2025, the gap between ambition and understanding became visible. The DeepSeek announcement, which centred on claims of highly capable AI models developed with significantly lower infrastructure cost than expected, triggered sharp market reactions. For some investors, it raised questions about whether hyperscalers were over-investing in compute capacity and whether capital deployment would generate the returns anticipated.

The announcement did not change the trajectory of AI. It did expose how fragile conviction can be when infrastructure investment, technical progress and commercial returns do not align neatly within a single reporting cycle.

Wall Street questioned why hyperscalers were deploying vast sums of capital without near-term returns. As scrutiny intensified, several hyperscalers reassessed near-term capital deployment, particularly in constrained markets such as the UK. That recalibration, driven largely by financial optics rather than demand fundamentals, was felt clearly across the UK data centre sector through parts of 2025.

And yet, despite that judder, Ark continued to grow. Not because we were insulated from the market, but because we were never dependent on a single interpretation of it.

Ark has always been built as a balanced business. Hyperscale matters, but it has never been the whole story. While new hyperscale commitments slowed, our government business continued to grow and deliver tangible value. Through Crown Hosting, Ark has supported the modernisation of a small but critical portion of the UK public-sector estate. That rationalisation of the legacy estate represents at least £9 billion in savings to the UK taxpayer, with the work delivered to date demonstrating both the feasibility and the scale of that opportunity. The limiting factor has never been capability. It has been focus, will and execution.

Our enterprise business secured meaningful new wins, and we continued to deliver on capacity already leased to hyperscale clients. At the same time, we made the decision to expand further into Europe, acquiring a new site in Barcelona.

In parallel, we moved decisively into neo-cloud, rapidly deploying AI-ready infrastructure for Nebius. The deployment supports one of the largest air-cooled, Blackwell GPU-based installations currently being brought online in Europe, delivered at pace without compromising resilience or performance. That outcome was not luck. It was the result of a world-class Ark team, built to partner closely with clients and equipped with the knowledge, mindset, tools and proven processes needed to deliver under pressure.

To understand where we are now, it helps to step back. Ten years ago, digital infrastructure felt like a well-defined inland lake. The boundaries were known. The conditions predictable. Cloud pushed us into a river, faster moving, less certain, but still directional. AI has taken us into the open ocean.

The boundaries are unclear, the conditions volatile and the scale unprecedented. Sovereign states are now investing at pace. Capital has become weaponised. Some players are well equipped for this environment. Others are not, and collisions are inevitable. Anyone claiming certainty about where AI is heading is wrong.

There are, however, things we can anchor to. Machine learning is not new. Inference will matter more than training in many regions. But beneath the surface sit profound uncertainties: new compute models such as quantum, new chip architectures, new materials, and new energy realities such as fusion, any of which could reshape how infrastructure is designed and built. This is not a moment for false bravado.

Despite the scale of change, the fundamentals still win. What has changed is how unforgiving the environment has become. Power is now the primary constraint. Location matters more than ever. Proximity to networks and population centres continues to define viable inference workloads.

The UK is currently unlikely, without major transmission network upgrades or policy shifts, to become a global centre for large-scale AI training. Power is simply too expensive. But inference, applied AI and research close to major metropolitan areas remain critical, provided the infrastructure exists to support them.

For Ark, this has not forced a pivot. It has validated our approach. We have sites in the right locations, with power already contracted, giving us a clear runway to grow the UK business beyond 700 megawatts. Ninety-five percent of Ark’s spend is returned to the UK economy, supported by long-standing UK-based partnerships across construction, engineering, steel, operations and services.

Through our hot-shell approach, clients retain the option for air, liquid cooling, or combinations of both, which in a fast-evolving market enables an iterative approach rather than forcing early, commercially irreversible decisions.

The Nebius deployment illustrates how expectations have shifted. Clients now expect speed, but not at the expense of resilience or performance. Delivering AI-ready capacity at pace, supporting Blackwell GPUs using air-cooled design, was not about chasing headlines. It was about execution and about demonstrating what readiness actually looks like. That means rapid commercial alignment, genuine partnership, swift commissioning, and staying close to clients as they stand up revenue-generating services quickly and efficiently.

For all the automation in this industry, infrastructure remains a people business. At Ark, culture has been built deliberately over more than a decade. People come to work because they want to. They care about what they do and who they do it with. Integrity and care cannot be taught.

Before Christmas, a customer told us they had never seen so many commissioning tags closed in such a short period anywhere in the world. That does not happen by chance. It happens when teams are aligned, trusted and accountable. Broken cultures do not survive moments like this. In uncertain times, focus on fundamentals and a world-class group of people becomes decisive.

The UK retains real advantages: a financial centre, world-class research, strong institutions and global relevance. Business remains simple. Revenue minus cost equals profit. When power accounts for half your cost base and is materially more expensive than in competing markets, you are at a disadvantage.

The UK suffers from a legacy of decades of under-investment in key infrastructure. Grid upgrades are underway but will take time. Pricing mechanisms remain outdated, and power subsidies are still under consideration. Training workloads have already moved elsewhere, and that trend will continue unless these fundamentals change.

The government rightly speaks of its ambition to become an AI powerhouse, but it remains anchored by its legacy estate. Through Crown Hosting, Ark and government have already demonstrated what modernisation can deliver. The opportunity is huge. Addressing just 10 percent of that legacy estate represents a £12 billion prize. The solutions are known and proven. What is missing is senior leadership, true engagement and vigorous execution delivered in a programmatic way. If something is critical and vital to our country’s future, it needs to be treated as such.

Looking ahead, 2026 will be one of Ark’s busiest years. In the UK, multiple sites are coming out of the ground. In Europe, Brussels is progressing rapidly, and Barcelona is ready to move, positioned at the centre of an emerging AI zone. Alongside this, neo-cloud continues to mature.

There is also Lonestar. Our partnership opens a new dimension of resilience. As climate risk and geopolitical uncertainty increase, off-planet data storage is moving from theoretical to practical. Satellite-based solutions are already being tested.

Nothing worthwhile is easy. These vast, uncertain seas are where capability is proven, where weak cultures fracture, and where exemplary execution matters. This is a moment of uncertainty, but also one of vast opportunity. Risk is fortune’s accomplice.

At Ark, we are focused on fundamentals, not the noise. The right sites. The right power. The right partners. The right people. The right partnering relationships with clients, because people do business with people. That is how you navigate these new waters. That is how you win.

And that is why 2026 feels less daunting than it does exciting.